Yahoo Sports

Yahoo Sports With Metalore Resources Limited (CVE:MET) It Looks Like You'll Get What You Pay For

Want to participate in a short research study? Help shape the future of investing tools and earn a $40 gift card!

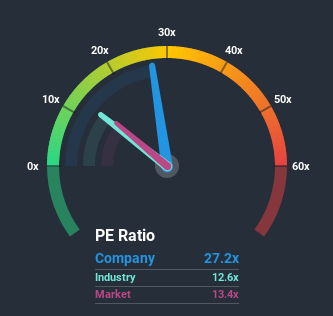

Metalore Resources Limited's (CVE:MET) price-to-earnings (or "P/E") ratio of 27.2x might make it look like a strong sell right now compared to the market in Canada, where around half of the companies have P/E ratios below 13x and even P/E's below 7x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

For instance, Metalore Resources' receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Metalore Resources

How Does Metalore Resources' P/E Ratio Compare To Its Industry Peers?

It's plausible that Metalore Resources' particularly high P/E ratio could be a result of tendencies within its own industry. You'll notice in the figure below that P/E ratios in the Oil and Gas industry are similar to the market. So we'd say there is little merit in the premise that the company's ratio being shaped by its industry at this time. Some industry P/E's don't move around a lot and right now most companies within the Oil and Gas industry should be getting restrained. Whilst this can be a heavy component, industry factors are normally secondary to company financials and earnings.

Although there are no analyst estimates available for Metalore Resources, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Metalore Resources' to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 37%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 2729% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

In contrast to the company, the rest of the market is expected to decline by 8.3% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this information, we can see why Metalore Resources is trading at a high P/E compared to the market. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse. However, its current earnings trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Final Word

The price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Metalore Resources revealed its growing earnings over the medium-term are contributing to its high P/E, given the market is set to shrink. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Although, if the company's relative performance doesn't change it will continue to provide strong support to the share price.

Plus, you should also learn about these 4 warning signs we've spotted with Metalore Resources (including 3 which are potentially serious).

If you're unsure about the strength of Metalore Resources' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.