Yahoo Sports

Yahoo Sports House rich and money poor: Deal with your debt, you've been warned

House rich and money poor Canadians are once again being urged to rein in their debt. The latest warning comes from Canada Mortgage and Housing Corporation.

CMHC says households with elevated debt are more vulnerable to higher interest rates, which would keep them from putting money into the economy or paying down debt. That assumes homeowners can keep up with mortgage payments.

“If an increasing number of borrowers begin to default on their loans, financial institutions may decrease lending activities in response.” says CMHC’s Brent Weimer. “These negative effects could then impact other areas of the economy.”

The global economy is showing signs of a slowdown. If a recession is around the corner, the Canadian impact could be magnified.

“Research has shown that recessions in highly indebted countries tend to exhibit a greater loss in output, higher unemployment, and last longer compared to countries with lower debt levels,” says Weimer.

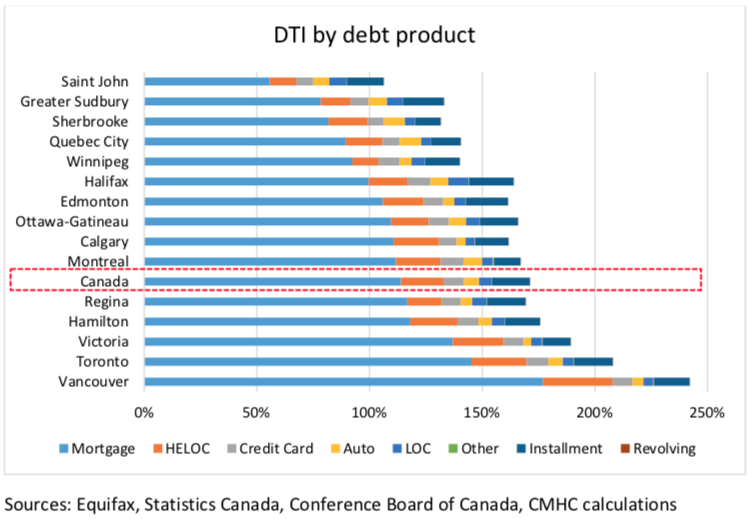

Debt relative to income has been trending higher. The average national debt-to-income ratio is hovering around a record high of $1.70 owed for every $1 earned. So the warning comes as no surprise to Credit Canada Debt Solutions CEO Laurie Campbell.

“Despite a reduction in overall mortgage debt on a macro level, individuals have been remortgaging their homes through HELOCs or taking out more mortgage debt than they can afford,” Campbell told Yahoo Finance Canada. “Add in the increasing interest rates and unsecured debt such as revolving high interest credit cards and it spells a recipe for disaster.”

Campbell expects the situation will only get worse in 2019.

Hot housing markets most at risk

Rising home prices in Vancouver and Toronto have caused the debt-to-income ratio to balloon the most, at 242 per cent and 208 per cent respectively. The ratio in Vancouver is more than double Saint John’s 106 per cent.

“The situation is one of the outcomes that flows from our tolerating home prices rising so much over recent decades, UBC professor Paul Kershaw told Yahoo Finance Canada.

Kershaw says we should also consider the flip side of the debt coin, which is wealth. As well as how it varies by age. He says older Canadians have been getting wealthier as a result of rising home prices and paid off mortgages, leaving the younger generation squeezed.

“For example the typical Canadian homeowner age 65+ has gained around $280k in wealth by comparison with the same age person in 1976 (after adjusting for inflation), and for every dollar of that additional wealth, s/he only took on an extra 7 cents in mortgage debt,” says Kershaw. “By contrast, the typical younger Canadian (under 35) has seen home ownership rates go down. So s/he isn’t accumulating wealth, and her consolation prize is rising rents.”

Kershaw says the wealth imbalance means fewer people can pay for medical care, other social programs, and benefits. He says taxing capital gains on principal residences could help level the playing field.

Download the Yahoo Finance app, available for Apple and Android.